When you’re working abroad, it can be difficult to calculate what your nett pay will be. There’s a lot of information about gross pay and deductions from gross pay. In this article, we break down the differences in gross vs nett pays for these countries: Singapore, Malaysia, Hong Kong, Vietnam, Philippines, Indonesia and Thailand. We also give some advice on how to best deal with taxes in different countries.

Gross pay is the amount that you’re paid before any deduction or tax. This would include your salary, allowances, bonuses and overtime payments.

Nett pay is what you will receive after all deductions have been taken out of your gross pay. Common examples of deductions include taxes, insurance premiums (health), social contributions etc. These factors make up for your ‘take home’ income which means how much money you actually get to keep in hand per month/ year.

In Malaysia (residents and non-residents) it works slightly differently where you will need to contribute to Employees Provident Fund (EPF), Social Security Organisation (SOCSO) and monthly tax deduction. The EPF was established to help employees save for a comfortable retirement by making voluntary contributions to the fund. You have the option of contributing at least 9% of your gross salary each month.

Employees who make contributions to SOCSO qualify for financial compensation in the case of work-related injuries and travel. For tax deduction, if your yearly employment income is more than RM34,000 (after EPF deductions), you must register a tax file and your employer may take a sum from your pay for monthly tax deduction payments.

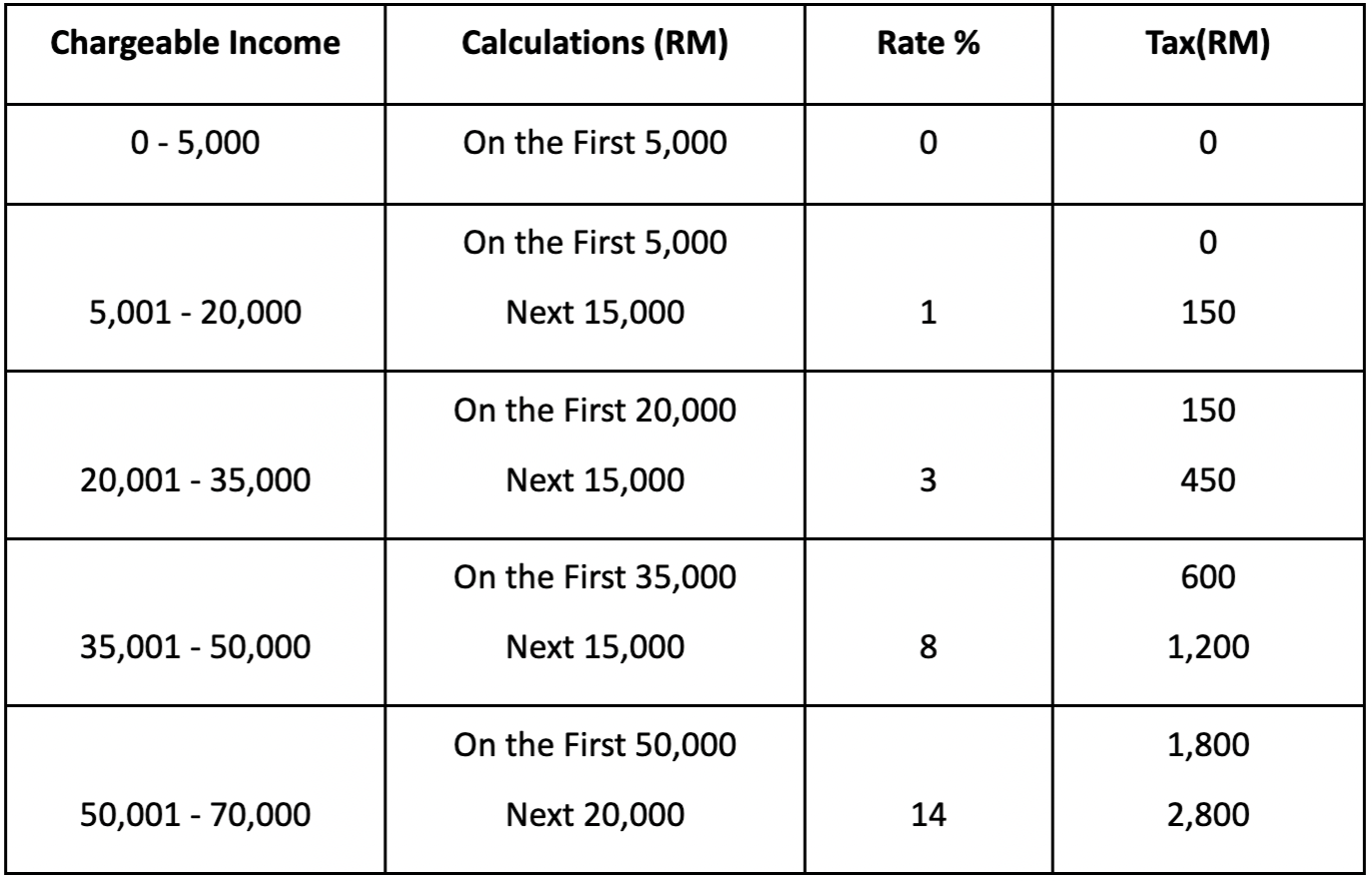

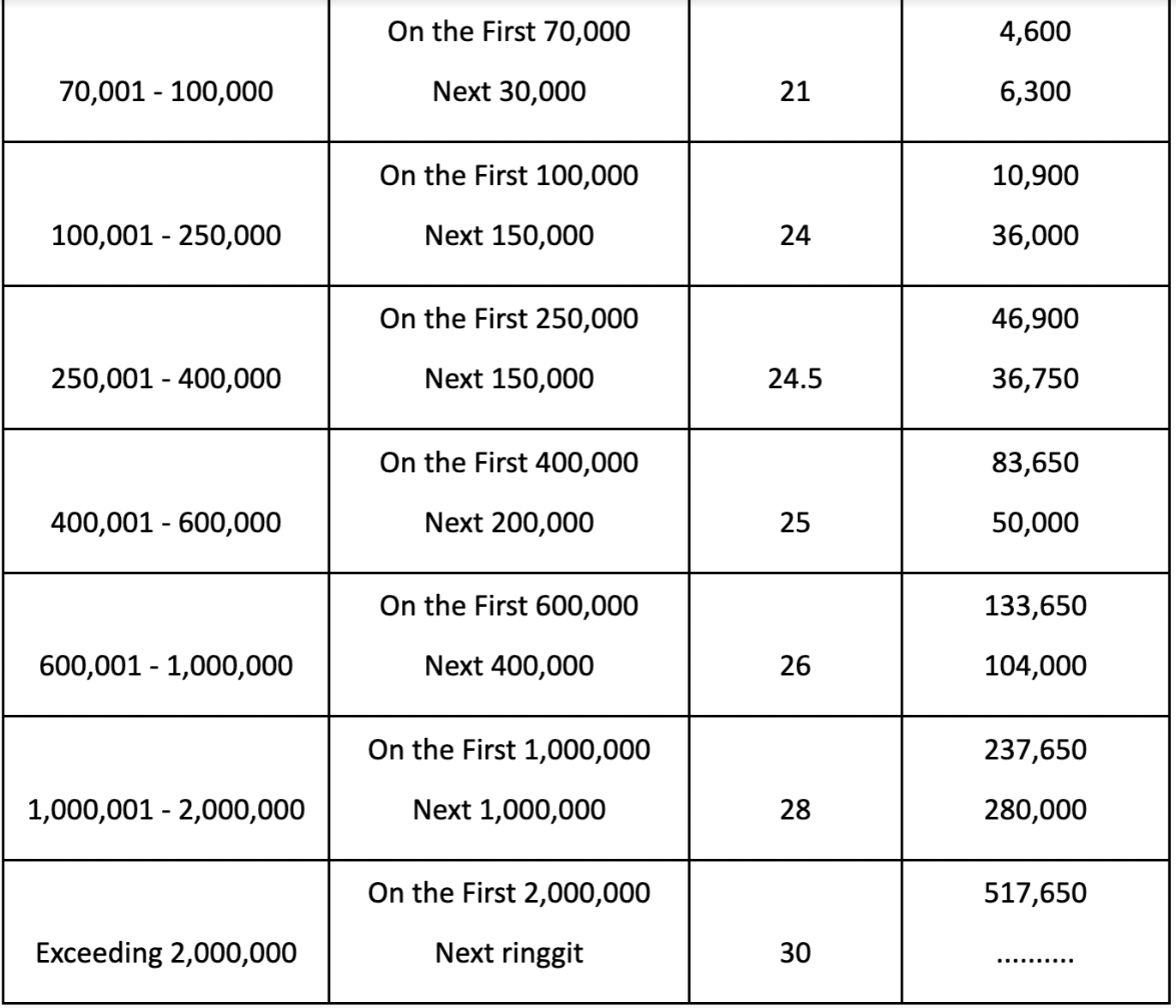

Lastly, for yearly tax payments, employees in Malaysia will have to submit yearly reports of gross pay earned during that year which includes foreign employment too. You will then be taxed accordingly, this is usually between 0-30% (If this amount exceeds the total monthly tax deduction, you will have to pay the balance amount in a lump sum at the end of the taxation year).

Here are some important details for deductions and tax rates.

Hong Kong, as a tax haven, has especially competitive income tax rates for non-residents and company taxes. Besides tax, employees and self-employed people must pay 5% of their wages to their MPF fund (Mandatory Provident Fund). Expatriates are not subjected to MPF if they enter Hong Kong to work for less than 13 months, or if they are members of an overseas retirement system.

Individual tax rates are progressive, with the net chargeable income (i.e. assessable income after deductions and allowances) taxed at a rate of 2% and up to 17%. Hong Kong’s tax system is based on a territorial principle. This implies that only income earned in Hong Kong is taxable there. However, income that has been taxed in another jurisdiction may be excluded from the salary tax in Hong Kong, and earnings earned outside of Hong Kong can also be considered non-Hong Kong sourced (exempted from Hong Kong salaries tax). Hong Kong salaries tax does not apply to income earned in the city by visitors who spend less than 60 days there.

Here are some important details for deductions and tax rates. This is a list of what you need to do if filing your taxes this year, so make sure that it’s in order!

i. Master Trust Schemes

ii. Employer-sponsored Schemes

iii. Industry Schemes

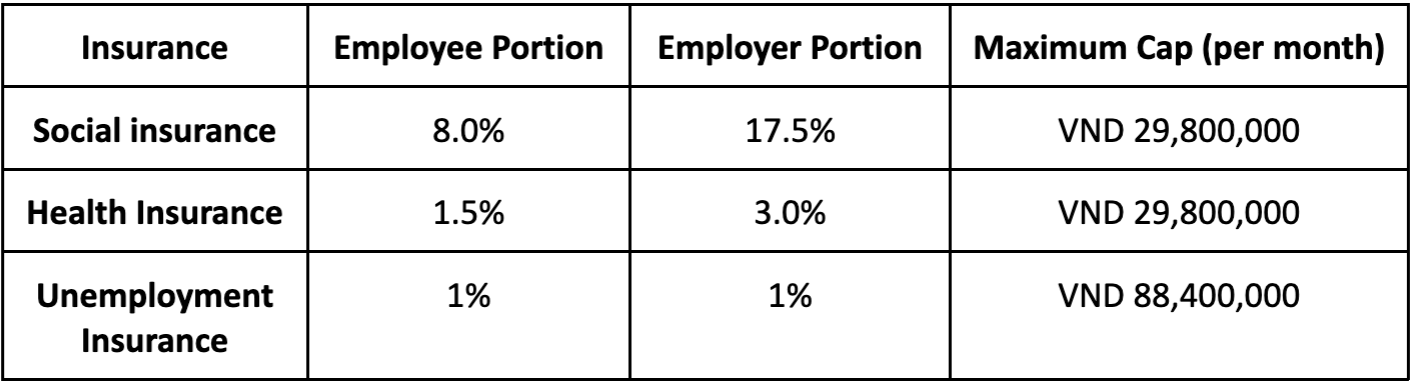

All Vietnamese citizens, including foreign workers who have resided in the country for more than six months, must contribute to the three systems. The following percentages must be paid by the employee: Social insurance (8%), health insurance (1.5%) and unemployment insurance (1%).

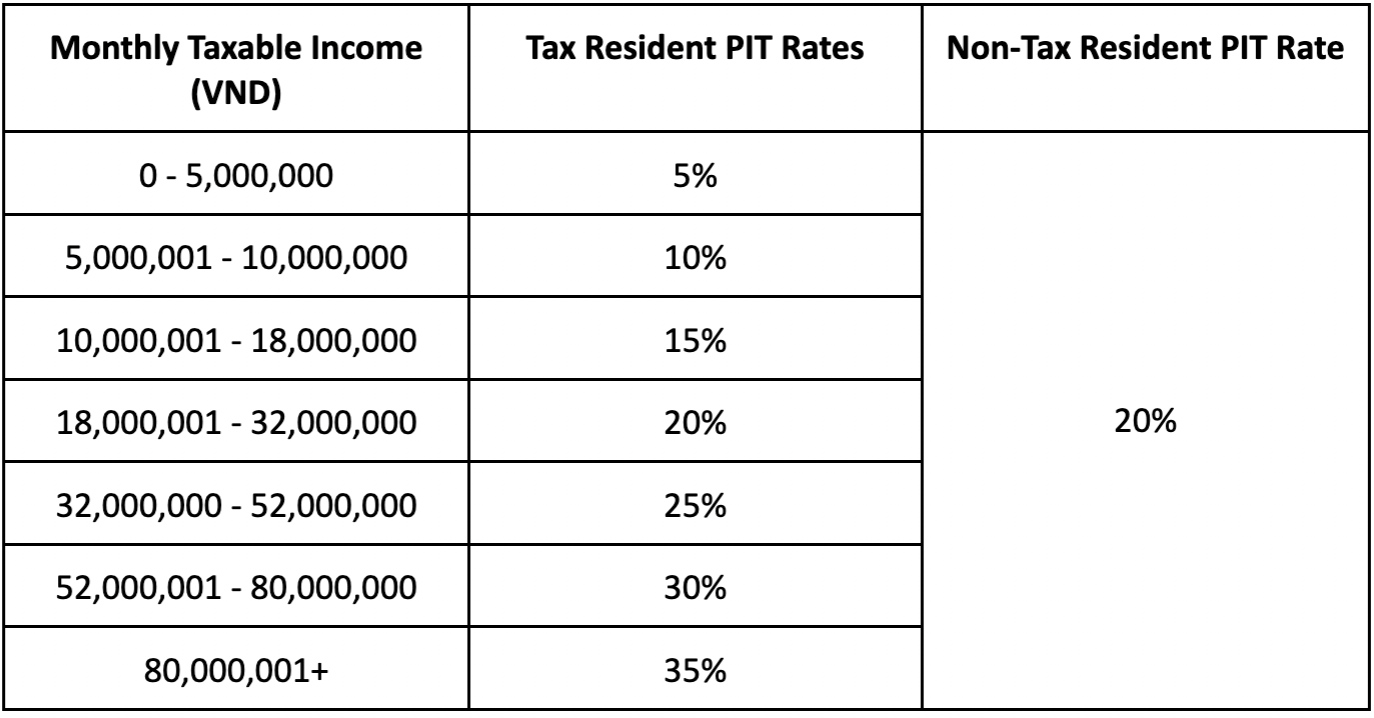

In Vietnam, Residents of Vietnam are taxed on their worldwide income, whereas non-residents are taxed on their Vietnam-sourced earnings only. The highest tax bracket in Vietnam is 35%, while taxes for non-residents are levied at a flat rate of 20%. Foreign currency income is converted to Vietnamese dong when calculating taxable income.

Here are the important details you need to know about deductions and tax rates.

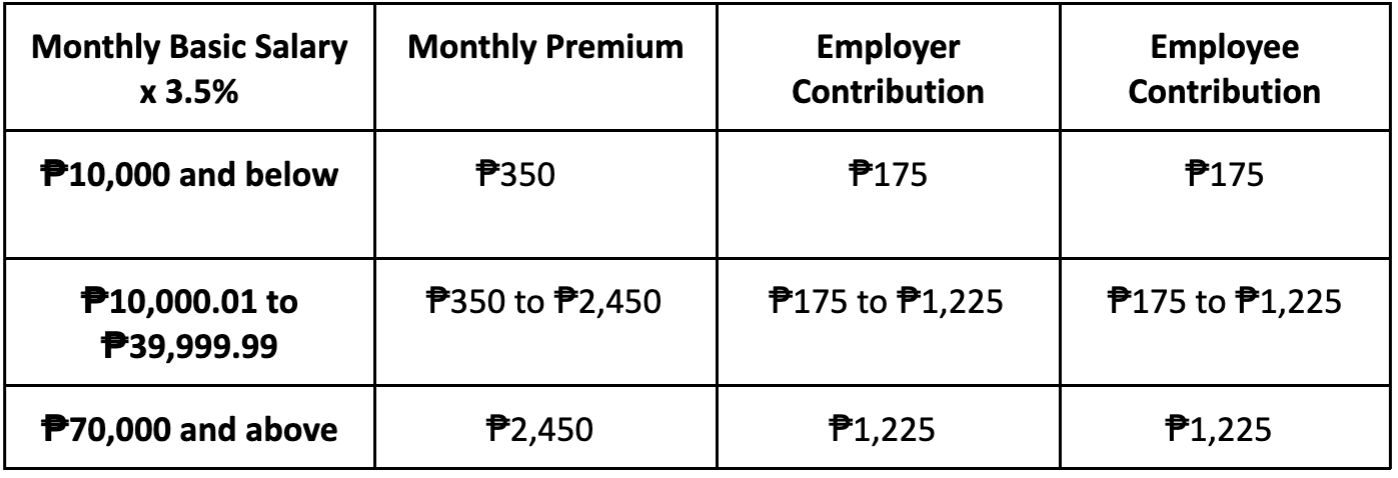

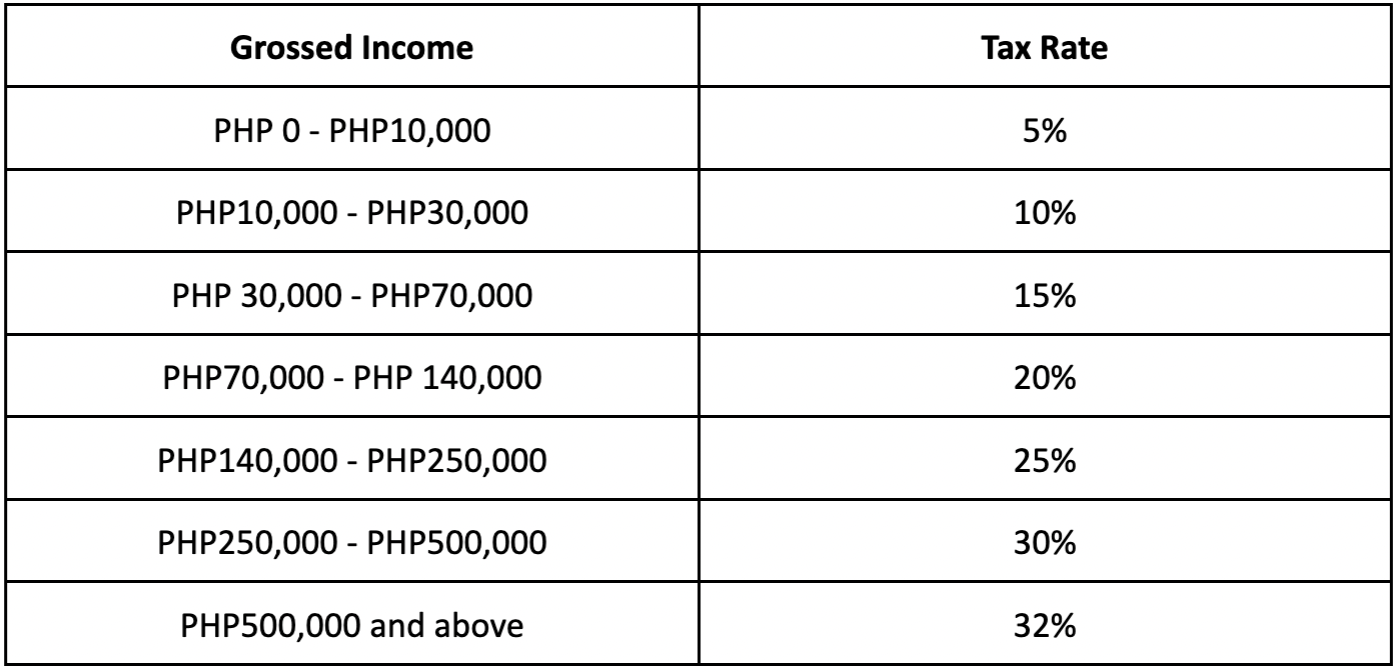

The Social Security System (SSS), the Home Development Mutual Fund (Pag-IBIG), and the Philippine Health Insurance Corporation (PhilHealth) provide social welfare services in the Philippines. Employers and employees are obliged by law to contribute to these organisations via payroll deductions as required by the Philippine Labour Code. The SSS contribution is 3.63% of an employee’s monthly salary. The Pag-IBIG fund has a monthly fixed contribution of ₱100. The employee’s wage is used to calculate the employee’s PhilHealth contribution. The employer must pay half of the premium and 50% of the monthly instalments will be taken out of the employee’s salary. The basic salary range is from ₱10,000 to ₱50,000 per month, which equals the minimal deposit of ₱275 and the maximum deposit of ₱1,375 each month.

The Filipino government taxes its citizens up to 32% no matter what their income is, regardless if it comes from the Philippines or not. Non-Filipinos are only taxed on any wages that have been earned while living there.

The deduction and tax in the Philippines is a complicated system, but it’s important for you to know the basics. Here we will break down your deductions and rates so that they make sense in context!

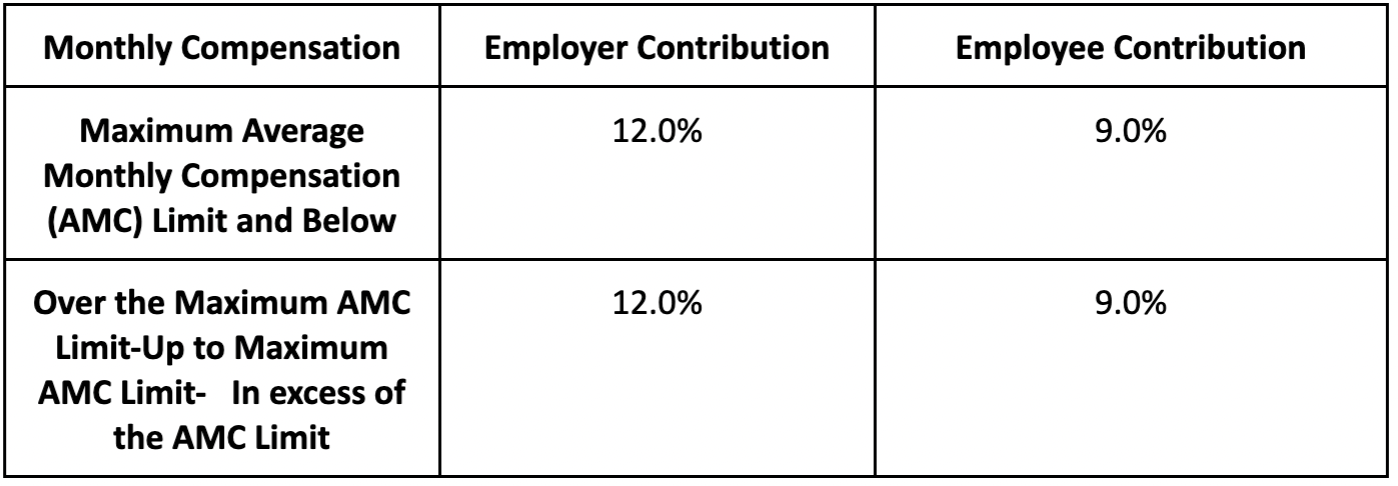

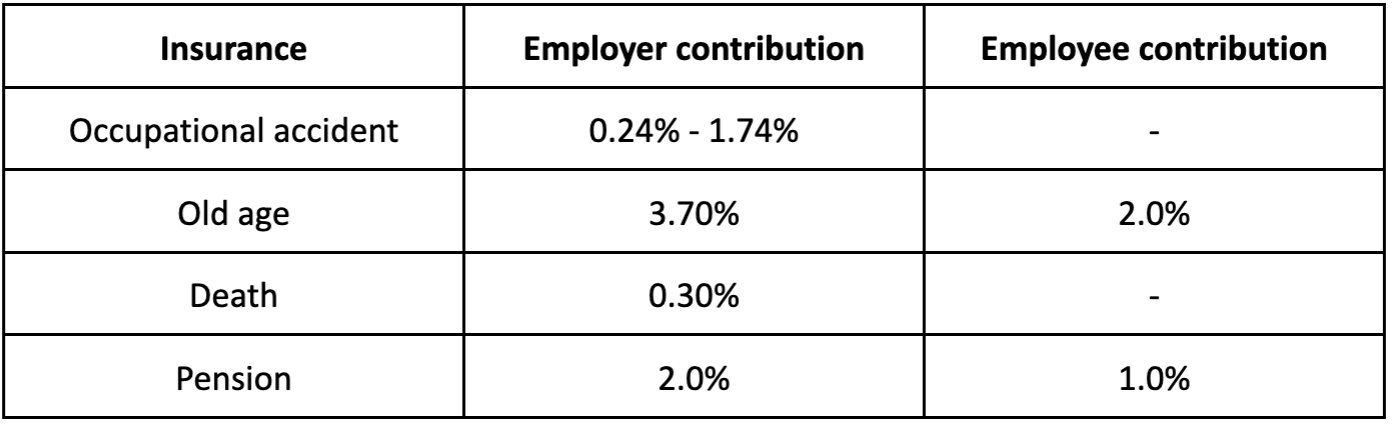

*due to Covid-19, the social security contributions will be at 12% for the meantime with the approval from The House of Representatives

In Indonesia, social security contributions are made in three different areas: Old age contribution (2%), healthcare (1%) and pension (1%).

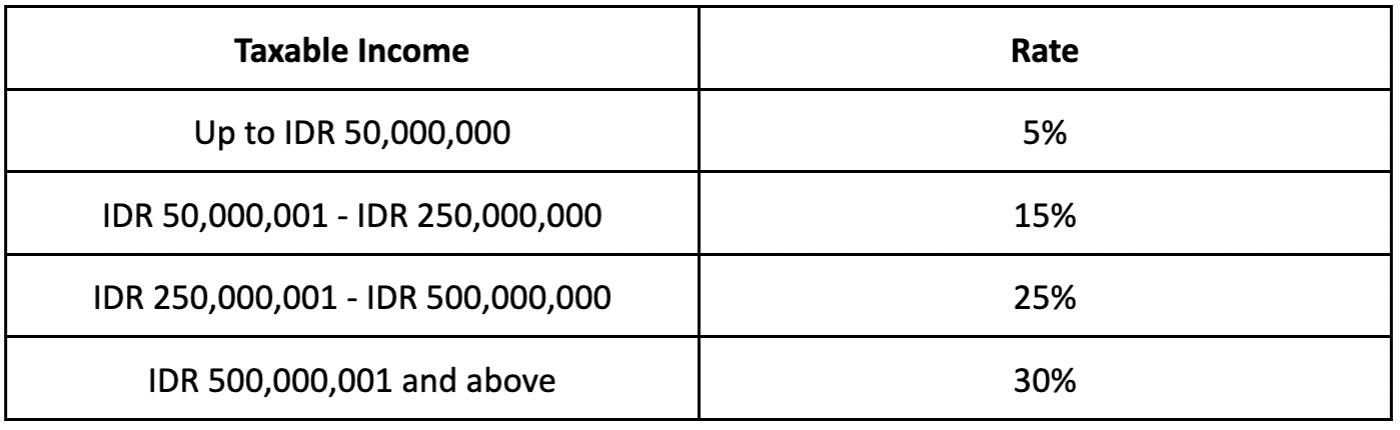

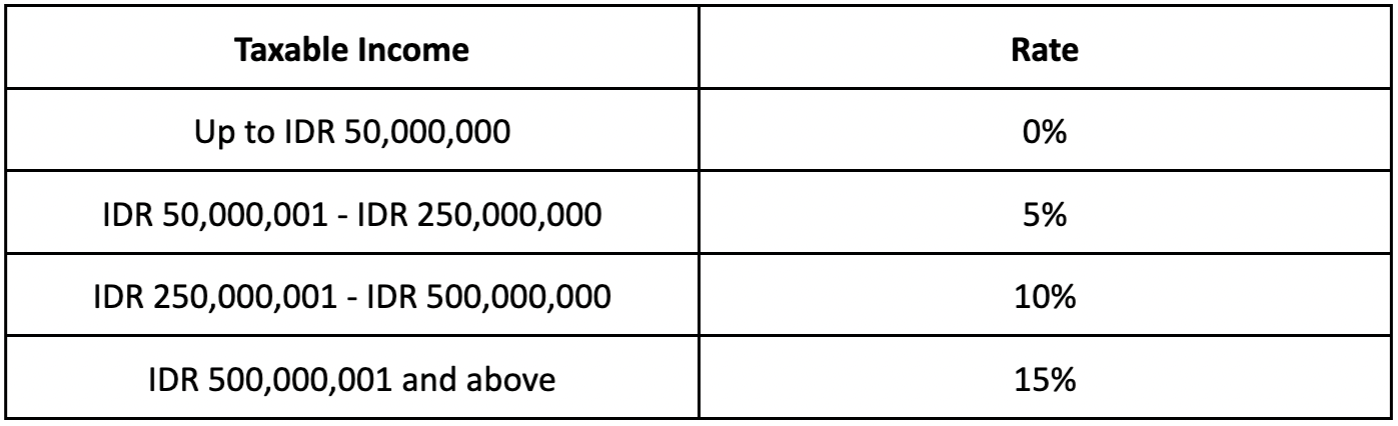

Resident citizens in Indonesia are taxed on their worldwide income, whereas non-residents are only taxed on locally sourced earnings. Non-resident employees are taxed with a general withholding tax of 20% on their income source within Indonesia.

Here are the important details you need to know about deductions and tax rates.

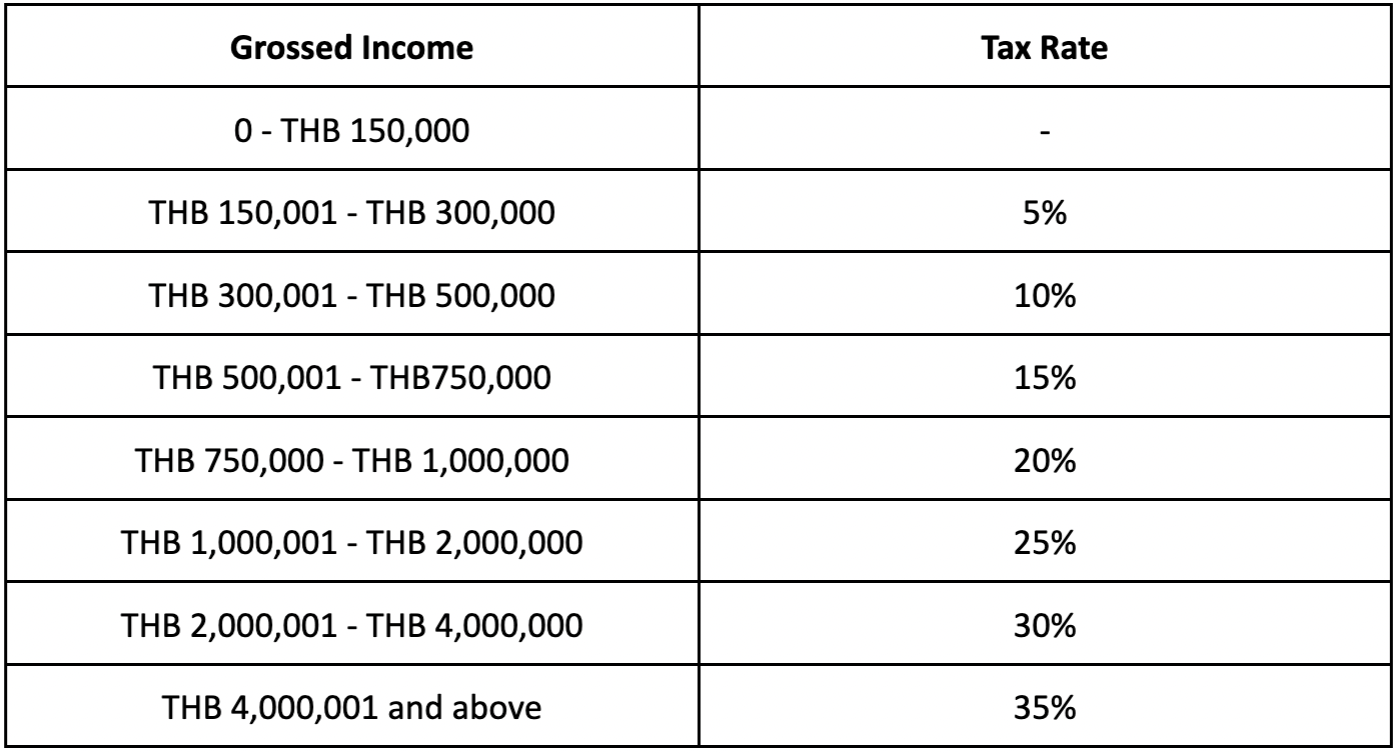

In Thailand, foreigners who don’t have an employment visa or work permit can only stay in the country for 90 days at one time before having to leave to renew their visas. If you’re staying longer than this then you will have to pay Thai personal income tax for the amount of time that exceeds 90 days, regardless of your salary is paid in Thailand or not.

There’s also a maximum allowance on what can be taxed but it varies depending on where you’re working and how much money per year is earned. Thailand has very high rates of taxation where foreigners who earn more than 800,00 baht/year automatically need to pay 30%. However, if they’re married to Thai nationals or earning less than that could get away with paying only 20%. Employees are also required to contribute 5% of their pay to Employee Social Security. The maximum monthly payment is 750 Baht.

Here are the important details you need to know about deductions and tax rates.

This would include:

There are several factors that can influence your take-home pay such as income tax, health insurance premiums, social security contributions etc. There isn’t too much of a difference in the amount you will receive if you were to compare gross vs nett pays with some examples listed above. However, we recommend getting advice from a tax consultant or accountant so they can help you understand how it works in your destination country. There’s no ‘one size fits all’ model when it comes to dealing with taxes and salary calculations for different countries, so working closely with a tax consultant or accountants would be the best way to go about it.

Some people think that it’s better to be paid on a gross basis as this means they will receive more money but the reality is often very different from what you might expect. Taxes and other deductions can make up for 50% of the total income which leaves you with little savings over time. No matter where in Asia or the world, always remember to keep track of all your expenses so that when tax season comes around again, you know exactly how much taxes need to be paid. We hope this article has been helpful by breaking down some differences between Gross vs Nett pays across a few different countries.